Are you on the fence about whether to buy a home right now? While the current mortgage rates may seem daunting, there are two compelling reasons why this might just be the perfect time to become a homeowner.

There’s been some confusion surrounding recent home price trends, but it’s important to look at the bigger picture.

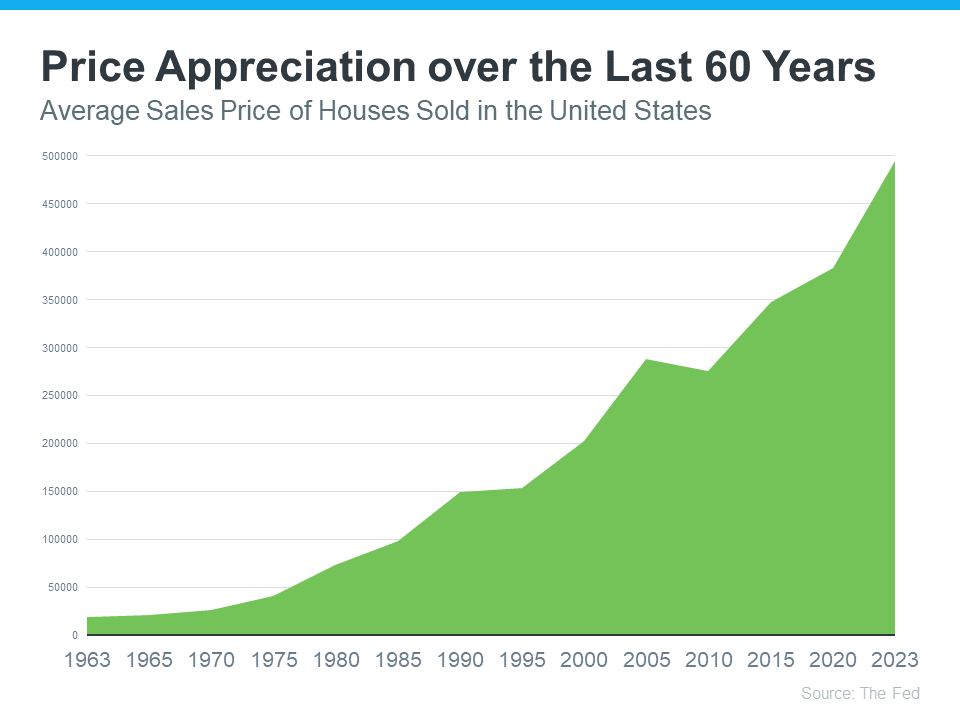

A Long-Term Upward Trend

Home prices may have had a few bumps, but the historical data from the Federal Reserve over the past 60 years shows a steady upward trajectory. This long-term growth can significantly benefit you as a homeowner.

Building Wealth Through Equity

As home prices rise, so does your equity. This is essentially money in your pocket. Over time, the equity you accumulate can significantly boost your overall net worth.

Protection Against Inflation

Owning a home can act as a hedge against inflation. While the value of money can erode over time, real estate tends to keep pace with or even outperform inflation, securing your investment.

Rent Keeps Going Up Through the Years

Renters are no strangers to the frustration of ever-increasing rent.

Escaping the Rent Hike Cycle

Rent prices have been steadily climbing for six decades, leading to financial stress for many. However, when you become a homeowner, you can lock in your monthly housing costs, bidding farewell to the relentless rent hikes. The stability this offers can be a game-changer.

Your Payments are an Investment

Your housing payments aren’t just expenses; they are investments. The choice is simple – do you want to invest in yourself or your landlord?

Homeownership vs. Rent

When you buy a home, you’re investing in your future, building equity and financial security. On the other hand, when you rent, that money is gone, never to return.

Conclusion

In the end, it all boils down to a fundamental choice: investing in your own future or contributing to your landlord’s wealth. As Dr. Jessica Lautz, Deputy Chief Economist and VP of Research at the National Association of Realtors (NAR), wisely states:

“If a homebuyer is financially stable, able to manage monthly mortgage costs and can handle the associated household maintenance expenses, then it makes sense to purchase a home.”

Bottom Line: Buying a home offers numerous benefits over renting, even in the face of high mortgage rates. If you wish to escape the relentless rent hikes and leverage the long-term appreciation in home values, it’s time to explore your options. Invest in yourself by becoming a homeowner.

Do you have more questions or doubts about buying versus renting? Here are some common questions:

FAQ 1: Is homeownership suitable for everyone?

Homeownership can be a wise choice if you’re financially stable and prepared for the responsibilities of maintenance and homeownership.

FAQ 2: How do I calculate if I can afford to buy a home?

Consider your income, savings, and current debts. Consult with a mortgage lender to determine a suitable budget.

FAQ 3: Are there any downsides to homeownership?

Homeownership entails responsibilities like maintenance costs and property taxes. It’s essential to budget for these expenses.

FAQ 4: How do I take advantage of rising home values?

Owning a home allows you to benefit from the long-term appreciation of property values, contributing to your wealth.

FAQ 5: Can I buy a home in a competitive housing market?

In competitive markets, work with a real estate agent to navigate bidding and find suitable options. It’s still possible to buy a home in such markets.