Rent or Buy: Is Renting Finally Cheaper? WOW!

Alright, here’s a head-scratcher for you. Fresh off the press, stats show that the average monthly mortgage in Kansas City rolls in at $2,188. That’s a cool 9.6% more than the $1,996 you’d fork out for rent. Quick math? Homeowners are shelling out an extra $192 every month, and that’s before we even chat about the extra costs of owning a home! So, with this logic, you’d think everyone would be renting, right? Yet, loads of folks in Kansas City are still leaning into buying. It makes you wonder… what’s the catch? Why are so many still chasing homeownership when renting seems to be the money-smart move at first glance? Trust me; there’s more to this story. Let’s dive in and crack this mystery wide open!

The Facts About Renting Vs Buying

On the surface, it might appear that the sole difference between renting and buying is monthly payments. But as you dig deeper, you’ll discover the true power of homeownership – equity. Let’s unravel the numbers.

Renting: A Straightforward Affair

Money to the Landlord:

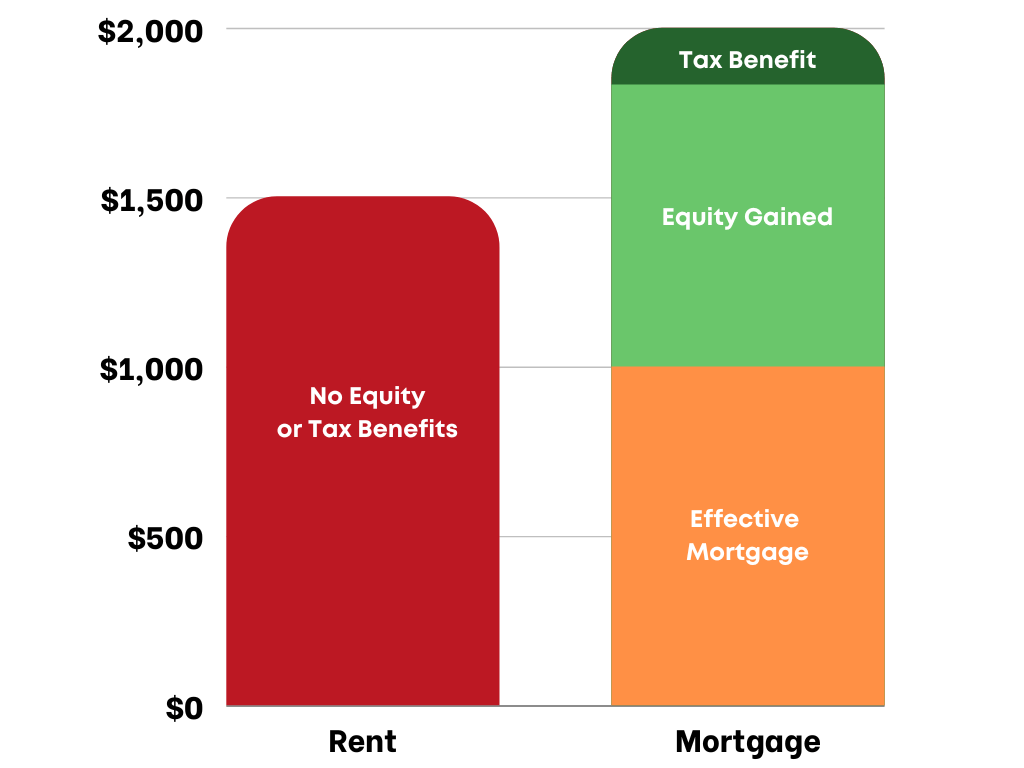

When you rent, every penny paid is a direct transaction to the landlord, offering you shelter but no long-term financial return.

BUYING: A DEEP-DIVE INTO HOMEOWNERSHIP

The Dual Nature of Your Payment:

While part of your mortgage payment is the interest, the other slice goes directly toward reducing your loan principal. This means with every payment, your debt decreases, and your ownership of the asset grows – this is ‘building equity’.

Appreciation in Value:

Over time, the real estate market has shown a tendency to appreciate. A $300,000 house could, given a 3% annual appreciation rate, balloon to over $400,000 in ten years.

Monthly Breakdown of Appreciation:

Dividing the $100,000 appreciation over ten years and then monthly, we’re looking at an equity gain of about $830/month. This isn’t money you see now, but it’s wealth being added to your portfolio.

Mortgage Minus Equity Gain:

With a $2,000 mortgage and subtracting the monthly equity gain, you’re effectively paying $1,170. Unlike renting, this amount takes into account the value you’re adding to your own asset.

Break down of monthly expense

TAX ADVANTAGES FOR HOMEOWNERS

Renting’s Tax Landscape:

Renting is simple but lacks in tax breaks. The monthly payment remains a fixed cost with no return on investment.

Homeownership’s Tax Perks:

One massive perk of owning a home is the tax deduction associated with mortgage interest. In the early years of the mortgage, a significant chunk of your payment is interest, which can be tax-deductible.

Tax Savings Illustrated:

Let’s say you’re earning $60,000 annually. If your interest payment in the first year is $10,000 and you’re in the 20% tax bracket, this could mean a tax savings of $2,000 annually or $166.67 monthly.

CONCLUSION

The decision to buy or rent isn’t merely about current expenditures. When comparing a $1,500 rent to a $2,000 mortgage, the real comparison becomes clear once equity and tax benefits are factored in. A homeowner effectively pays closer to $1,000, considering the monthly equity gain and tax benefits, proving that homeownership is not just about shelter but also building wealth over time.

Mortgage Rates Climbing – Time to Act Fast

FAQS

- Why does everyone keep talking about equity when buying a home?

Equity represents your ownership in the home. As you pay down your mortgage and as your property appreciates, your equity grows. (learn more about home equity here!) - How does the real estate market’s appreciation benefit homeowners?

Over time, a property’s value tends to rise. So, homeowners not only build equity through payments but also benefit from the home’s value increasing. - Are there any tax benefits for renters?

Renters don’t benefit from tax deductions related to mortgage interest or property taxes, which homeowners can claim. - How is the effective mortgage payment lower than the actual amount paid monthly?

By considering the equity gain and tax benefits, homeowners effectively pay less than their monthly mortgage suggests. - Is the equity gained through appreciation liquid?

No, it’s realized when you sell the property or tap into it through methods like home equity loans. - If I’m planning to stay in a city for just a few years, is it better to rent or buy?

If you’re planning to live somewhere for a short duration, renting might be more advantageous. The costs associated with buying and then selling a home (like closing costs, realtor fees, and potential market fluctuations) can make it less economical for short-term stays.